Forex & CFD Leverage Explained: 30:1, 500:1 and How to Actually Use It

A clear, honest guide to leverage in forex and CFD trading — what it really does, how 30:1 and 500:1 compare, and why position sizing matters more than the number on your account.

By René Balke

Leverage is one of the most talked-about and most misunderstood parts of forex and CFD trading. You’ll see brokers advertising everything from a conservative 30:1 to a headline-grabbing 500:1, and most explanations treat the bigger number as either a shortcut to riches or a guaranteed way to blow up your account.

Both takes miss the point. Leverage isn’t good or bad — it’s a tool, and like any tool, the outcome depends entirely on how you use it. This guide walks through what leverage actually does, how the different levels compare, and the one principle that separates traders who use it well from those who don’t.

What leverage really is (and how margin fits in)

Leverage lets you control a larger position than your own capital would normally allow. Your broker effectively fronts the rest, and the slice you put up to open and hold the trade is called margin.

The relationship is simple:

Required margin = Position size ÷ Leverage

Higher leverage doesn’t change the trade — it changes how much of your money is tied up to hold it. In percentage terms:

- 30:1 leverage → you post about 3.33% of the position as margin

- 500:1 leverage → you post about 0.2% of the position as margin

A useful analogy is a property deposit. To control a €300,000 apartment you don’t pay €300,000 up front — you put down a deposit and control the whole asset. Leverage works the same way: a small, refundable margin lets you control a much larger position in the market.

A concrete example

Say you want to trade 0.1 lot of EUR/USD — a position worth roughly $10,000.

| Leverage | Margin required | Capital left free (on a $1,000 account) |

|---|---|---|

| 30:1 | ~$333 | ~$667 |

| 500:1 | ~$20 | ~$980 |

Scale it up to a full standard lot (a $100,000 position) and the contrast is even clearer: that trade needs about $3,333 in margin at 30:1, but only $200 at 500:1.

This is the genuine, practical advantage of higher leverage — capital efficiency. The same position ties up far less of your account, leaving the rest free. Used sensibly, that flexibility is exactly why experienced and professional traders often prefer higher leverage: it lets them hold positions without locking up capital they’d rather keep available.

Try it yourself: the live leverage simulator

The simulator below runs the exact maths from this article in real time. Drag the sliders — account balance, position size, leverage and market move — and watch required margin, free margin, margin level and the stop-out point respond instantly. The two columns compare a regulated 1:30 account with a professional / offshore 1:500 one side by side, and switching the instrument to gold or an index pulls live prices.

The one idea that changes everything: leverage ≠ risk

Here’s the part most explanations get backwards.

Leverage does not determine how much you can lose. It only sets your margin requirement. What you can actually lose on a trade is determined by your position size and how far the price moves — not by the leverage number on your account.

Look again at that EUR/USD example. If the price moves 50 pips against a 0.1-lot position, you lose about $50 — whether you opened it at 30:1 or 500:1. The leverage changed how much margin was tied up; it did not change the loss by a single cent.

Once this clicks, leverage stops looking scary and starts looking like what it is: a setting that controls capital efficiency, sitting in the background while your position size does the real work.

Margin, margin level, and what happens when a trade goes wrong

Your broker continuously tracks your margin level:

Margin Level = (Equity ÷ Used Margin) × 100

As open trades move against you, your equity falls and that percentage drops. Two thresholds matter:

- Margin call (often around 100%) — a warning. The broker asks you to add funds or reduce exposure.

- Stop-out (often around 50%) — the broker automatically closes positions to prevent the account going further into the red.

The more of your available margin you’ve committed, the faster you reach these levels. This is the mechanism behind most account blow-ups — and it’s worth understanding clearly, because it points straight to the real risk.

Where traders actually get hurt: oversizing, not leverage

If leverage doesn’t change your loss on a given trade, where does the danger come from?

It comes from using the freed-up margin to open oversized positions — what’s sometimes called the “free margin trap.”

Because 500:1 leverage requires so little margin, it leaves most of your balance showing as “free.” The temptation is to treat that free balance as room to open much bigger trades. Here’s what that looks like on a $1,000 account:

- 0.1 lot, 50 pips against you → −$50 (5% of the account)

- 1.5 lots, the very same move → −$750 (75% of the account)

The leverage didn’t cause that second outcome. The oversized position did. The same trader, at the same leverage, sizing sensibly, would have been completely fine. High leverage simply gives you more rope — it’s up to you whether that rope is useful slack or something you trip over.

This is why blaming leverage for losses is misleading. The skill isn’t avoiding leverage; it’s controlling position size.

Why regulated jurisdictions cap retail leverage at 30:1

In the EU (under ESMA), the UK (FCA), and Australia (ASIC), retail leverage on forex is capped at 30:1. It helps to be clear about what this cap actually is: a blunt, one-size-fits-all guardrail. By lowering the ceiling, regulators indirectly limit how large a position a small deposit can open — which, as we’ve seen, is the thing that actually drives risk. It’s an external brake applied to everyone, whether they want it or not — useful if you specifically want that limit imposed on you, and simply something to work around if you don’t.

Importantly, the cap isn’t a flat 30:1 across everything. It’s tiered by how volatile the instrument is:

| Leverage | Instrument |

|---|---|

| 30:1 | Major currency pairs |

| 20:1 | Minor pairs, gold, major indices |

| 10:1 | Other commodities, minor indices |

| 5:1 | Individual stocks |

| 2:1 | Crypto |

(In Germany, BaFin adopted these ESMA measures permanently.)

Alongside the lower leverage, regulated retail accounts come with two consumer protections worth knowing about:

- Negative balance protection — you can’t lose more than you deposited. If a sharp market gap blows past your stop, the broker absorbs the difference.

- Investor compensation schemes — if the broker itself becomes insolvent, a scheme reimburses eligible client funds up to a cap.

That second one is widely misunderstood, so it’s worth a closer look.

What is an “investor compensation scheme”?

An investor compensation scheme is a statutory safety net that pays you back — up to a limit — if a regulated broker goes bankrupt and can’t return the money or assets it was holding for you.

The key distinction: it covers broker failure, not trading losses. If you lose money on a bad trade, nothing reimburses that. The scheme only steps in if the firm collapses and your funds aren’t where they should be.

In Germany, the relevant scheme is the EdW (Entschädigungseinrichtung der Wertpapierhandelsunternehmen). It covers 90% of an eligible claim, up to a maximum of €20,000 per investor, and that ceiling applies to your total claim against the firm regardless of how many accounts you hold. It’s overseen by BaFin.

Don’t confuse it with a deposit guarantee scheme, which protects cash deposits at a bank (typically up to €100,000 per person, per bank). Different scheme, different trigger.

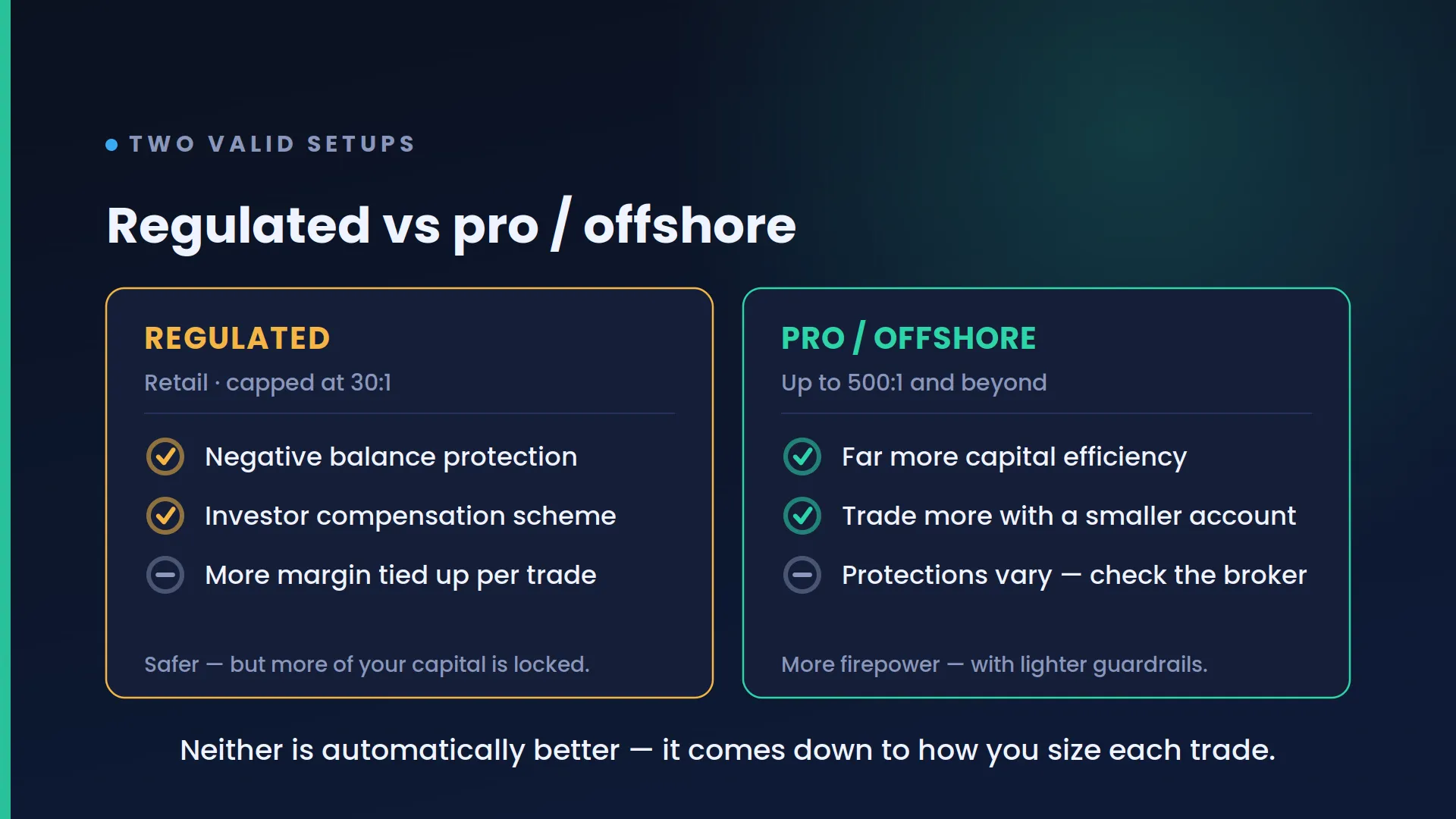

The three setups: regulated, professional, and offshore

There isn’t one “correct” leverage level — there are different setups suited to different traders. Here’s a transparent side-by-side:

| Regulated retail | Professional client | Offshore | |

|---|---|---|---|

| Typical max leverage | 30:1 | Up to 500:1 | 500:1 and beyond |

| Best suited to | Traders who want a built-in limit on themselves | Experienced traders who qualify | Traders who want full flexibility |

| Capital efficiency | Lower | High | High |

| Negative balance protection | Yes (retail) | Not guaranteed | Varies — verify with broker |

| EU investor compensation | Yes (e.g. EdW) | Reduced / varies | Typically outside EU schemes |

| Qualification needed | None | Must meet criteria | None |

A few notes to read this fairly:

Professional status is available inside the EU/UK if you qualify — typically by meeting two of three conditions: a portfolio (cash plus instruments) over €500,000, around 10 significant trades per quarter over the past year, or at least a year working in the financial sector in a relevant role. Clearing that bar unlocks higher leverage, but you waive some of the retail protections in exchange — that’s the deliberate trade-off you’re accepting.

Offshore brokers (regulated in jurisdictions such as Seychelles or Mauritius) offer high leverage to ordinary clients with no qualification needed, plus generally fewer restrictions on how you trade. Many serious traders use them precisely for that flexibility. The honest trade-off is that they usually sit outside EU/UK compensation schemes, and consumer protections like negative balance cover can vary — so the sensible move is simply to check the specific broker’s terms before funding an account, rather than assuming the protections are identical to a domestic retail account.

None of these is automatically “better.” A regulated retail account gives you a thicker safety net at the cost of capital efficiency; a professional or offshore account gives you efficiency and flexibility while asking you to take on more of the responsibility yourself. The right choice depends on your experience, your capital, and how you trade.

How professional traders actually use leverage

Notice what experienced traders don’t do: they don’t pick a broker based on who offers the biggest number.

They start from a different question — “How much of my account am I willing to risk on this one trade?” Usually a small, fixed amount, often 1–2%. From there it’s arithmetic: given where their stop sits, what position size keeps the loss inside that 1–2%? They size the position to the risk first. Leverage then simply determines how much margin sits locked up behind it — ideally a small fraction, leaving a comfortable buffer.

Used this way, whether the account is set to 30:1 or 500:1 barely affects the outcome. The leverage number becomes almost irrelevant — which is exactly the sign it’s being used correctly.

The bottom line

Leverage is a power tool. It doesn’t make the market move faster, and it doesn’t decide your losses — it decides how efficiently your capital is used. Higher leverage frees up more of your account; lower leverage forces a built-in margin of safety. Both are valid; the danger only appears when free margin gets turned into oversized positions.

So instead of asking “how much leverage should I use?”, ask “how much am I risking per trade?” Get the position sizing right, and the leverage takes care of itself — at any level.

Ready to put it into practice? Browse the brokers we use and recommend — regulated 30:1 and professional / offshore 500:1 accounts, with leverage, protections and account types compared side by side.

Risk note: nothing in this post is investment advice. Trading forex and CFDs carries significant risk. Past performance is no guarantee of future results.